A Nigerian’s Guide to Proof of Funds for Canada

So, you're planning your move to Canada. One of the most critical steps you'll face is showing your "Proof of Funds," or POF. What is it, really? Simply put, it's the evidence you provide to the Canadian government that you have enough money to settle in and support yourself and your family when you first arrive.

For anyone coming from Nigeria, think of it this way: it’s your financial welcome mat, your "settlement savings" to show you can cover your initial living costs in cities like Toronto or Calgary before you start earning in Canadian Dollars.

Understanding Proof Of Funds For Your Canadian Dream

Let's call Proof of Funds your "settlement savings." This is the money that Immigration, Refugees and Citizenship Canada (IRCC) needs to see to be confident that you can manage life in Canada right from the start. It’s not about proving you're rich; it's about proving you're prepared.

Picture this: you're moving from Abuja to Lagos for a new opportunity. You'd need money set aside for your first month's rent, transportation, and feeding before that first salary comes in. The proof of fund for Canada works on the exact same principle, just scaled for a new country. It’s your financial safety net for those first few crucial months.

More Than Just Naira in The Bank

The IRCC isn’t just glancing at your final bank balance. They're digging a bit deeper to check for two very important things: legitimacy and availability.

- Legitimacy: Where did this money come from? You have to show its origin. A large, unexplained lump sum of several million Naira appearing in your account right before you apply will raise immediate red flags.

- Availability: How quickly can you get to this money? Funds locked away in real estate in Lekki, vehicles, or complex business shares don't count. The money needs to be liquid and accessible for you to pay for rent or groceries tomorrow.

This requirement is a cornerstone of many immigration programs. For those learning how to apply for Express Entry Canada, getting the proof of funds right is absolutely essential for most streams. The idea is to present a stable financial picture that tells the visa officer you’re a responsible and well-prepared candidate.

The core idea behind POF is straightforward: Canada wants to be sure new immigrants can get on their feet without facing immediate financial distress. It's a practical measure of your readiness for this new chapter.

Why It’s A Non-Negotiable Step

Getting the POF wrong is, unfortunately, one of the most common reasons a Canadian permanent residency application is rejected. The Canadian government needs assurance that you can support yourself and anyone coming with you. For immigration streams like Express Entry, you must show you have enough unencumbered funds to cover basic living expenses.

The exact amount you need is tied directly to the size of your family. With a bit of foresight and the right documents, this is a perfectly manageable part of your journey that helps pave the way for your new life.

Calculating Your Required Settlement Funds

Alright, let's get down to the numbers. Figuring out exactly how much money you need to show is where your planning really begins. This isn’t just a random figure—it’s a specific amount set by Immigration, Refugees and Citizenship Canada (IRCC), and it’s tied directly to the size of your family.

Nailing this calculation from the get-go is essential. It helps you avoid any last-minute financial chaos and ensures you confidently meet one of the most critical requirements when it's time to submit your application.

Who Counts as Family?

First things first, we need to be clear on who IRCC considers "family" for this purpose. It’s not just about who is physically moving with you. The count includes:

- You (the main applicant)

- Your spouse or common-law partner

- Your dependent children

- Your spouse's or partner's dependent children

Here's a detail that often trips people up: you must include these family members even if they aren't coming to Canada with you. So, if you're married with two kids but you're planning to immigrate alone initially, you still need to prove you have enough funds to support a family of four.

Real-World Examples for Nigerian Applicants

Let's put this into perspective with a few common scenarios you might find yourself in. Remember, IRCC sets these figures in Canadian Dollars (CAD), so you'll be working with the Naira equivalent.

- The Single Professional: Imagine Ade, a banker from Lagos, moving to Toronto on his own. He only needs to show funds for one person. If the current requirement is CAD $14,690, his goal is to have the Naira equivalent of that amount ready.

- The Young Couple: Bisi and Tunde from Abuja are recently married and embarking on this journey together. They need to calculate their funds for a family of two. If the threshold is CAD $18,288, that’s the magic number they need to hit.

- The Family of Four: The Okoro family from Port Harcourt—a couple with their two children—are all making the move. They must show proof of funds for four people, which, based on current figures, would be around CAD $28,183.

These numbers are updated every year, so it's vital to check the official IRCC website for the latest requirements before you finalise anything. As you move forward, creating an Express Entry profile is a major milestone, and having a clear picture of your required funds is a huge part of being ready.

The Naira Exchange Rate and Your Financial Buffer

For anyone in Nigeria, the Naira-to-CAD exchange rate is a huge variable you can't ignore. The Naira’s value can be volatile, which introduces a level of risk to your application. One day your funds might be comfortably above the required amount, but a sudden dip in the exchange rate could push you below the line without warning.

To guard against this, a smart move is to keep 10-15% more than the minimum required amount in your account. This extra cushion is your financial safety net.

Think of this buffer as your insurance policy. It protects you from:

- Sudden Naira Devaluation: A sharp drop in the Naira's value won't put your application in jeopardy.

- Bank and Transfer Fees: When you eventually move your money, international transfer fees and bank charges will eat into the total.

- Unexpected Delays: If your application process drags on, this buffer ensures your funds remain compliant over time.

Taking this small extra step can save you a world of stress. It shows the visa officer that you're not just scraping by but are a financially responsible candidate who is truly prepared for a new life in Canada.

What IRCC Accepts as Valid Proof of Funds

Now that you know how much money you need, let's get into the part where the details really matter: what kind of proof will IRCC actually accept? Getting this wrong can unfortunately bring your entire application to a halt, so it’s vital to get it right from the start.

The golden rule from Immigration, Refugees and Citizenship Canada (IRCC) is that your settlement funds must be liquid and readily accessible. Think of it this way: you need to be able to use this money the moment you land in Canada for things like your first month's rent or a trip to the grocery store. It can't be tied up in anything that takes time to sell or convert into cash.

The Official Bank Letter: Your Most Crucial Document

The single most important document you’ll submit is an official letter from your Nigerian bank, printed on the bank's letterhead. This isn’t your everyday account statement. It’s a specific document that must contain very precise information for the visa officer.

Your letter must clearly show the following:

- The bank's full contact information (address, phone number, and email).

- Your full name and address.

- A list of all your current or savings accounts, along with the account numbers.

- The date each account was opened.

- The current balance of each account.

- The average balance for the past six months.

That last point—the six-month average balance—is extremely important. It shows the visa officer that the money has been sitting in your account for a while and wasn't just borrowed and deposited yesterday to meet the requirement. It’s all about demonstrating a stable financial history, which builds trust and credibility.

What Absolutely Does Not Count as Proof of Funds

It’s just as crucial to know what IRCC will flat-out reject. Many of us in Nigeria have our wealth tied up in various assets, but for immigration purposes, most of these won't work because they aren't liquid.

Do not try to use any of the following as your proof of funds for Canada:

- Real Estate: Land, houses, or any other type of property.

- Vehicles: The value of your car or other vehicles is not accepted.

- Company Shares or Stocks: These are investments and are not considered liquid enough.

- Cryptocurrency: Digital currencies like Bitcoin are too volatile and are not recognised as settlement funds.

- Borrowed Money: This is an immediate red flag. Loans from family, friends, or banks just for your proof of funds are strictly forbidden and can lead to a misrepresentation finding, which carries severe consequences.

The core principle is simple: if you can't quickly and easily access it as cash to pay for your living expenses in Canada, it doesn't count. Your proof of funds must be unencumbered money that you personally control.

Using Joint Accounts and Other Things to Keep in Mind

What if the money is in a joint account with your spouse? That's perfectly fine, as long as your name is on the account. You have legal access to the funds, which is exactly what IRCC needs to see. If your spouse isn’t coming with you to Canada, it’s a good idea to include a signed letter from them authorising you to use the money for your settlement.

The rules are strict for a reason—they ensure a transparent and fair process. Nigerian applicants must provide bank statements covering at least 6 months, supported by that official letter we talked about. Your bank must confirm the account opening date, current balance, any outstanding debts, and those all-important average balances. This is all part of Canadian law to prove you legally own and can access the funds.

Beyond just the type of funds, you should also be aware of any relevant foreign asset reporting requirements that might apply to ensure you’re being fully transparent about your global financial situation. At the end of the day, your goal is to present a clear, legitimate, and accessible financial picture.

How to Properly Document a Gift Deed

https://www.youtube.com/embed/SRaxYRj9L3I

In Nigeria, it's common for family—parents, aunties, or uncles—to support our biggest dreams. Getting a financial gift to help with your proof of funds for Canada is a perfect example. But here's the catch: to an IRCC officer, a large sum of money suddenly appearing in your account looks like a major red flag. A simple bank transfer won't cut it; you have to prove it's a genuine gift, not a loan you have to pay back.

This is where a Gift Deed becomes absolutely essential. It’s a formal, sworn document that creates a solid paper trail, proving the money is yours to keep, with no strings attached. If you skip this step, the visa officer might think the money is just a loan in disguise or that it was temporarily "parked" in your account to meet the requirement. That suspicion could put your entire application at risk.

Crafting an Airtight Gift Deed Letter

A proper Gift Deed isn't just a casual letter; it's a legal affidavit. In Nigeria, this means it needs to be sworn before a legal authority, like a Notary Public at a court. This simple act adds a layer of authenticity that IRCC takes very seriously. Remember, the letter must be written by the person giving you the money (the "donor").

Here’s exactly what the donor needs to put in the letter:

- Donor's Full Details: Their complete name, address, and how they're related to you (e.g., "Father," "Aunt").

- Your Full Details: Your full name and relationship to them.

- The Gift Amount: The exact amount of money given, clearly stated in both Naira and Canadian Dollars.

- The "No Repayment" Clause: This is the most important part. The letter must state very clearly that the money is an irrevocable gift and there is no expectation of repayment whatsoever.

- Donor's Signature: The letter has to be signed and dated by the donor.

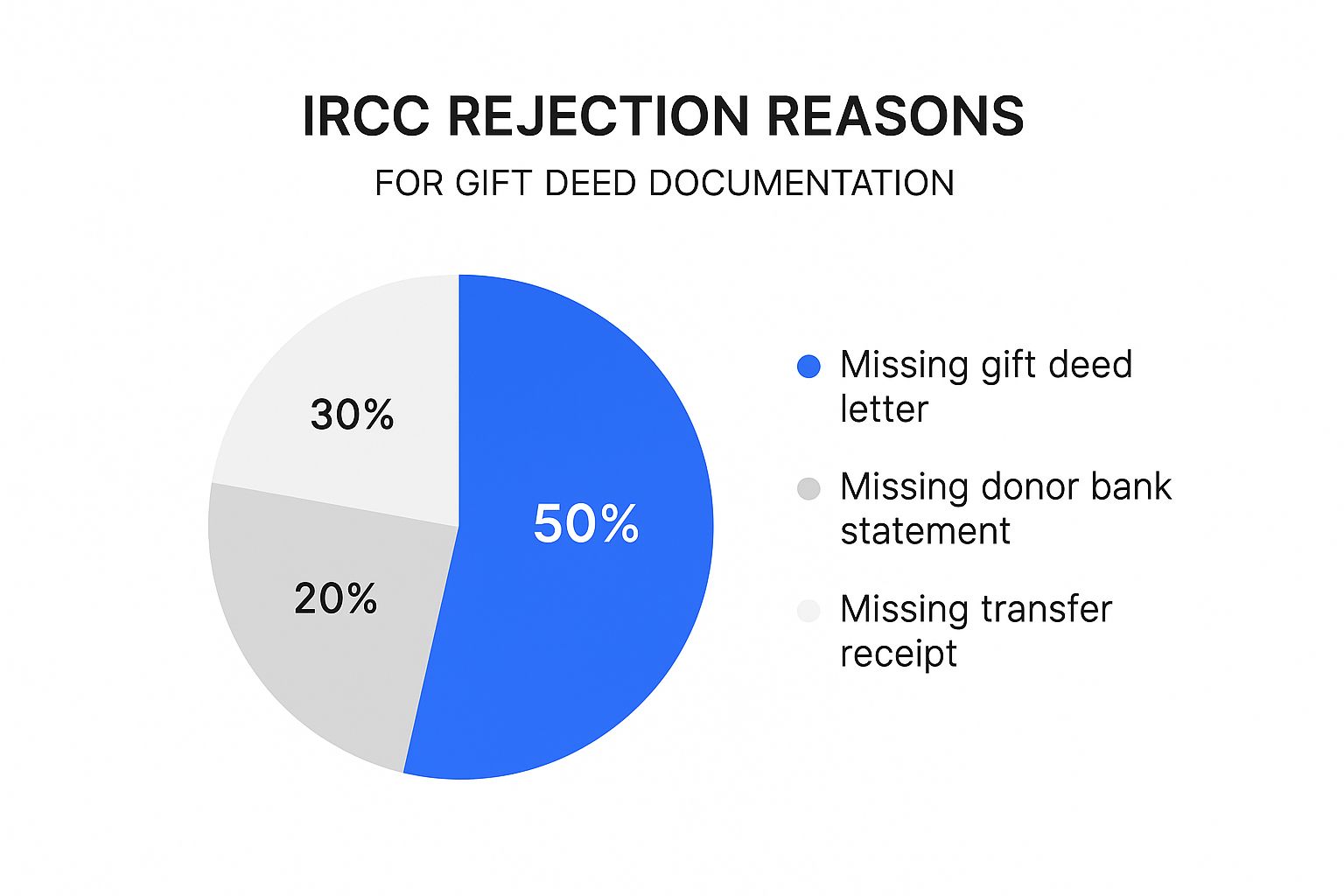

This infographic breaks down the most common reasons IRCC rejects gift deed documents, showing just how crucial each piece of the puzzle is.

As you can see, a staggering 50% of rejections happen simply because the gift deed letter itself is missing. That makes it the single most critical document you need to get right.

Completing the Paper Trail

The sworn letter is the star of the show, but it can't stand alone. To give the visa officer the full picture, you need to show the money's complete journey from the donor to you. This means the donor has to provide their own supporting documents too.

Think of it like a detective story where you have to provide all the clues. The Gift Deed is the confession, and the bank statements are the forensic evidence that backs it up, leaving no room for doubt.

Your donor must provide a copy of their bank statement showing the funds leaving their account. This transaction must perfectly match the amount written in your Gift Deed. Finally, you'll include the receipt or proof of transfer showing the money landing in your account.

When you put these three things together—the sworn Gift Deed, the donor's bank statement, and the transfer receipt—you create a transparent, undeniable record. This kind of thoroughness eliminates suspicion and makes your proof of funds solid, showing IRCC that you're a serious, well-prepared applicant.

Common POF Mistakes Nigerian Applicants Make (And How to Fix Them)

Learning from other people's mistakes is one of the smartest things you can do on your journey to Canada. When it comes to your proof of funds, a few common errors trip up Nigerian applicants time and time again, leading to frustrating delays or even application refusals.

Let's walk through these common pitfalls. Knowing what they are beforehand will help you put together a financial profile that is clear, credible, and exactly what the Canadian immigration officers are looking for.

Sudden Large Deposits Out of Nowhere

This is probably the biggest red flag you can raise. Picture this: your bank account has been sitting at around ₦2 million for months, then—boom!—a deposit of ₦15 million lands just a week before you ask for your proof of funds letter. To an immigration officer, this looks like you borrowed the money just to meet the requirement, a practice they call "funds parking."

Often, this money is completely legitimate. Maybe you sold a plot of land in Lekki or your car to gather the funds. The money is truly yours, but without the right paperwork, it looks suspicious.

To an immigration officer, undocumented money has no history. Your job is to provide a clear, verifiable story for every large sum that enters your account, transforming suspicion into confidence.

You have to create a solid paper trail for any unusually large deposit.

- Sold a car? You'll need the signed Deed of Assignment (or deed of sale), the change of ownership papers, and proof of payment from the buyer.

- Sold property? Make sure you have the executed Deed of Assignment, evidence of the buyer's payment, and any other relevant sales documents.

Letting Your Balance Dip Below the Minimum

This is a critical error that can torpedo your application. The proof of funds requirement isn't just a one-time thing; you need to keep that minimum balance from the day you submit your application right up until you land in Canada.

Life happens, we all know that. An emergency might pop up. But if your balance drops below the required amount—even for a single day—your application could be refused if IRCC happens to request an updated statement at that exact moment.

A good rule of thumb is to always keep a buffer of about 10-15% over the minimum required amount. This protects you from currency swings and unexpected costs, and it shows the officer that you’re financially stable, not just scraping by.

Using Funds That Aren't in Your Name

The rule here is simple: the money has to be in an account that belongs to you or you and your spouse jointly. You can't just use a bank statement from your parents, siblings, or a friend, even with their permission. The money has to be legally yours and available to you at all times.

If a family member gives you money as a gift, it must be properly documented with a legal Gift Deed, as we've covered. The money must then be transferred into your personal bank account to be counted. Submitting someone else's bank statement is an automatic non-starter.

Submitting an Incomplete Bank Letter

A lot of Nigerian banks use a standard template for reference letters, but these often miss the specific details that IRCC requires. Handing in one of these incomplete letters is an easy mistake to make and just as easy to avoid.

A basic letter showing only your current balance won't cut it. You need to politely (but firmly) insist that your bank includes every single one of the following details on their official letterhead:

- Your full name and the bank's contact information

- A list of all your account numbers

- The date each account was opened

- The current balance of each account

- The average balance over the last six months

If your bank manager seems unsure, it's a good idea to bring a sample letter showing them exactly what's needed. An incomplete letter forces the visa officer to fill in the blanks, and they won't bother—they'll just move to reject the application.

To help you spot these issues early, here’s a quick guide to some of the most frequent errors we see and how to handle them.

Common Proof of Fund Errors and Solutions

| Common Mistake | Why It's an IRCC Red Flag | How to Avoid or Fix It |

|---|---|---|

| "Funds Parking" | A large, sudden deposit without explanation suggests the money might be borrowed and not genuinely yours. | Provide a complete paper trail for every large transaction: sales agreements, deeds of sale, or gift deeds. |

| Balance Drops Below Minimum | Shows financial instability and failure to meet the requirements throughout the application process. | Maintain a 10-15% buffer above the minimum required amount to cover currency changes and small expenses. |

| Funds Not in Applicant's Name | The money is not considered accessible to you, even with permission from the account holder. | Funds must be in your name or a joint account with your spouse. If gifted, it must be legally transferred to your account with a Gift Deed. |

| Missing 6-Month Average | The officer cannot see your financial history or verify that the funds have been stable over time. | Insist your bank includes the 6-month average balance for each account in the official proof of funds letter. |

| Using Unacceptable Assets | Assets like real estate, vehicles, or cryptocurrency are not considered liquid and cannot be used for settlement. | Liquidate these assets and deposit the cash into your bank account well in advance. Keep all documentation of the sale. |

Taking the time to double-check these details ensures that your proof of funds is strong, clear, and meets every one of IRCC's requirements, paving the way for a much smoother application process.

Your Final Proof of Funds Checklist

Alright, this is it. Your final action plan before you hit that submit button. I've boiled down everything we've covered into a simple checklist you can scan through. Let's use this to give every single document one last look.

Think of this as the final once-over to make sure your financial profile is not just good, but completely convincing. Getting this part right is a massive step toward your new life in Canada.

The Essential Pre-Submission Review

Before you even dream of uploading a single file, run through these foundational checks. Trust me, spending a few minutes here can save you from common slip-ups that lead to frustrating delays.

- Confirm the Latest Fund Requirements: Head straight to the official IRCC website. Double-check the current settlement fund amounts required for your specific family size. These numbers can and do change, so don't ever rely on old information.

- Calculate Your Buffer Zone: Do you have at least 10-15% more than the minimum? This buffer is your safety net against currency fluctuations (hello, Naira!) and it demonstrates good financial planning to the visa officer.

- Verify Account Holder Names: Make sure every single account is in your name, or a joint account with your spouse if they are coming with you. Money in your parent's, sibling's, or friend's account simply won't be accepted.

Your Document Checklist

With the basics squared away, it’s time to get your hands on the paperwork. Every document you submit tells a piece of your financial story. Your job is to make sure that story is complete, clear, and consistent.

Think of your submission like an exam where you have to show all your work. A missing document is like an incomplete answer—it can lead to a failing grade on your application.

Here is your final document checklist:

- The Official Bank Letter: Does your letter from the bank have everything? I’m talking about your name, the bank’s contact info, all account numbers, the date each account was opened, the current balance of each account, and the six-month average balance. If any of these are missing, it's not ready.

- Six Months of Bank Statements: Have you gathered a complete, unbroken set of statements for the last six months? No gaps, no missing pages.

- Documentation for Large Deposits: Got any large, unusual sums of money that showed up in your account? You need a clear paper trail. This could be a signed Deed of Assignment for a car or property sale, or a sworn Gift Deed.

- Gift Deed Paper Trail (If Applicable): If a gift is part of your funds, you need all three pieces of the puzzle:

- The sworn Gift Deed letter from the person who gave you the money.

- The donor's bank statement showing the funds leaving their account.

- The transfer receipt confirming the money landed in your account.

Ticking off every item on this list will give you the confidence that your proof of funds is rock-solid. For more guidance on the entire journey, you can relocate to Canada from Nigeria with a clear roadmap.

Got Questions? We’ve Got Answers

When it comes to proving your settlement funds, a few common questions always seem to pop up. Let's tackle some of the most frequent ones we hear from Nigerian applicants so you can navigate these specific issues with confidence.

Can I Use My Nigerian Pension Funds?

This is a big one. Many people wonder if their pension savings can count as proof of funds. The straightforward answer is almost always no.

IRCC needs to see funds that are liquid and completely accessible to you from day one in Canada. Your pension is locked away until retirement, so it doesn't meet this standard. The only exception is if you’ve recently withdrawn a lump sum from your pension. In that case, you can use the money, but you’ll need to provide rock-solid documentation of the withdrawal to show exactly where that large deposit came from.

What If My Bank Won't Give Me the Right Letter?

It's a frustrating but common scenario in Nigeria. You ask for a proof of funds letter, and your bank hands you a generic reference that's missing half of what IRCC needs to see. Don't just accept it.

You need to be persistent. The best approach is to prepare your own sample letter listing every required detail: your full name, all account numbers, the date each account was opened, the current balance, and the all-important six-month average balance. Bring this with you, speak directly with the bank manager, and politely insist they reproduce it on official letterhead. They may have to calculate the average manually, but an incomplete letter is a huge risk for your application.

Do not walk out of that bank with a letter that doesn't tick every single box for IRCC. A missing detail like the six-month average balance is one of the most common—and completely avoidable—reasons applications get delayed or even rejected.

How Long Does the Money Need to Stay in My Account?

This is critical, so listen up: the required funds must stay in your account from the moment you submit your application all the way through to the moment you land in Canada.

Immigration officers can ask for an updated proof of funds at any stage of the process, including when you arrive at the airport. If you've spent the money, they can refuse your application or, in the worst-case scenario, turn you away at the border. The money is for your settlement, so don't touch it until you've settled.

Can I Use My Spouse’s Account If They Aren't Coming with Me?

If the money is in a joint account that has both your names on it, you're good to go. Because your name is on the account, you have legal access to the funds. That said, it's a smart move to also get a signed letter from your spouse confirming you have their permission to use the full amount for your move to Canada.

However, using an account that is only in your spouse's name is a bad idea. It just adds a layer of complication that you don't need. Keep it simple: make sure the settlement funds are in an account with your name on it, whether it's yours alone or a joint one.

Planning a move to Canada is a massive undertaking, and getting reliable information is key. That's where JapaChat comes in. As Nigeria’s first AI immigration expert, it's built to give you instant, accurate answers to your questions. Forget relying on secondhand advice. Get the clarity you need to plan your journey with confidence. Sign up for free on JapaChat today and take control of your immigration process.

Leave a Reply