Proof of Funds Canada: Essential Guide for Nigerian Immigrants

Navigating Proof Of Funds Canada: A Nigerian Perspective

When you start your Canadian visa application, proof of funds Canada often feels like a major hurdle. Seeing high figures on the Immigration, Refugees and Citizenship Canada (IRCC) list can cause stress—especially when you’re comparing naira to dollars at the airport. Understanding why Canada requires this financial buffer turns confusion into a clear checklist.

Conversations with Nigerians who secured permanent residence reveal one key point: some programs require bank statements, while others waive the rule if you have a job offer. You might find this useful: Check out our guide on How to Master Relocation to Canada from Nigeria.

Immigration Pathways And Exemptions

When you review the main immigration streams, keep these rules in mind:

- Federal Skilled Worker Program (FSWP) and Federal Skilled Trades Program (FSTP) require proof of funds unless you hold a valid job offer.

- Provincial Nominee Programs (PNPs) under Express Entry follow federal guidelines—funds are needed if you don’t qualify under Canadian Experience Class.

- Canadian Experience Class (CEC) applicants and those with an arranged employment offer are exempt from this requirement.

| Program | Proof Required? | Exemption Condition |

|---|---|---|

| Federal Skilled Worker (FSWP) | Yes | Valid Canadian job offer |

| Federal Skilled Trades (FSTP) | Yes | Arranged employment permit |

| Provincial Nominee Program (PNP) | Conditional | Under CEC or with job offer |

| Canadian Experience Class (CEC) | No | — |

Demystifying The Financial Threshold

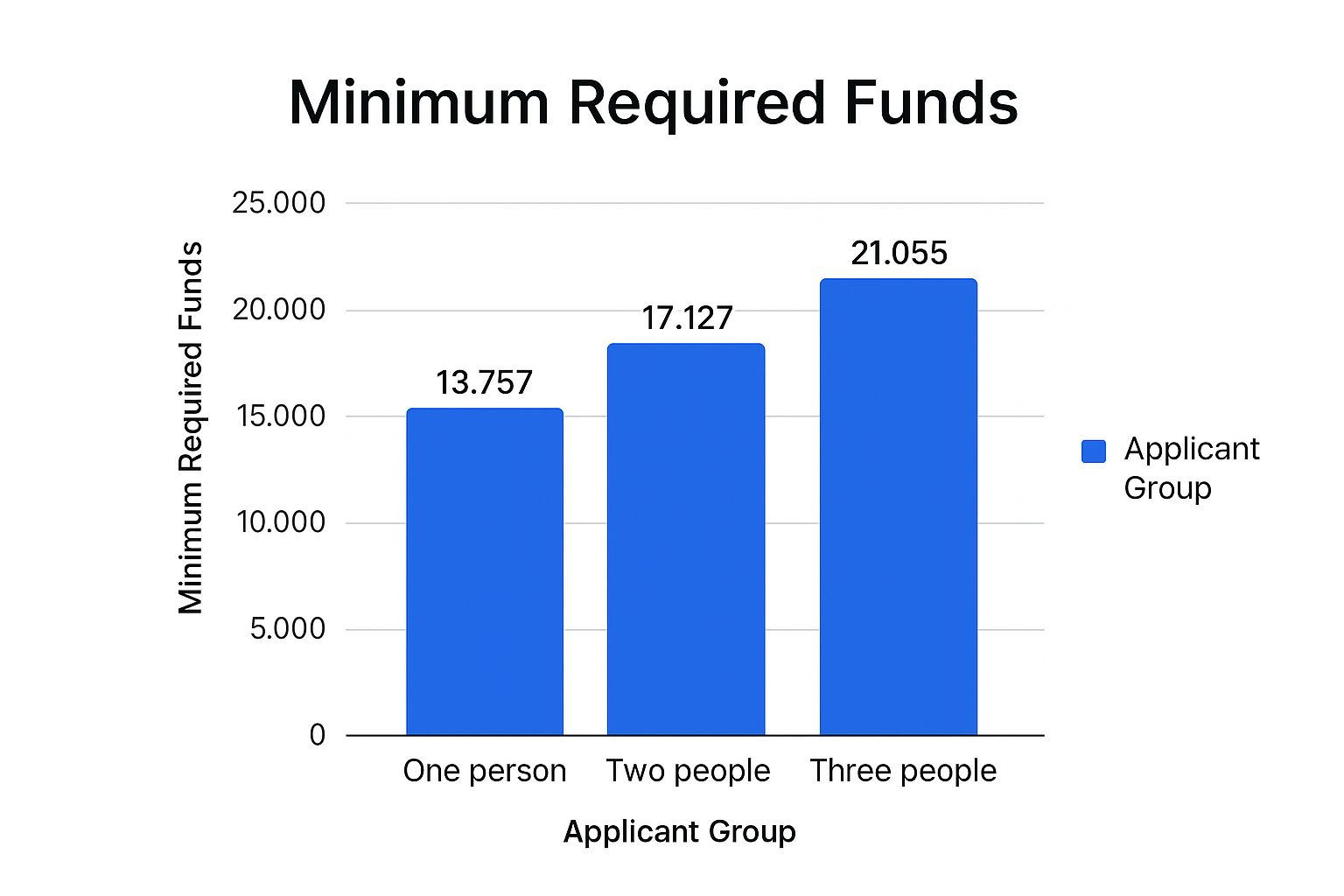

Each year, Canada adjusts the minimum savings based on 12.5% of low-income cut-off figures from Statistics Canada. As of May 2024, you must show at least $14,690 CAD for a single applicant, $18,288 for two people and $22,483 for three. This requirement ensures newcomers can manage basic living expenses when they arrive. Discover more insights about proof of funds here.

Psychological Impact And Common Misconceptions

Facing the proof-of-funds rule often brings a wave of worry over naira-to-dollar conversions. Common myths include:

- Assuming family-pooled savings count without separate statements.

- Believing large recent deposits won’t be flagged.

- Overlooking that visa officers expect a six-month average balance in your bank letter.

Understanding these pitfalls helps you approach your application with confidence and prevents unexpected delays.

By breaking down each requirement, you’ll be ready to convert Canadian figures into today’s naira and build a solid savings plan.

Breaking Down the Financial Thresholds for Nigerians

Below is a data chart that visualizes the proof-of-funds requirements for Express Entry in Canada, showing the required Canadian dollars alongside their Naira equivalents. This chart highlights how the funding threshold rises with each additional family member.

The bar chart makes it clear: a single applicant needs ₦11.8 million, while a family of four must show nearly ₦22 million. Each extra member adds roughly ₦3.5–₦4.0 million to your savings target.

Canada’s proof of funds Canada requirement often surprises Nigerians once they translate the figures into Naira. Breaking these amounts down by family size brings clarity on how much you really need to save.

Proof Of Funds Requirements By Family Size

A detailed breakdown of the minimum funds required for different family sizes when immigrating to Canada, with equivalent amounts in Nigerian Naira

| Family Members | Required Funds (CAD) | Approximate Naira Equivalent |

|---|---|---|

| 1 | 14,690 | ₦11,752,000 |

| 2 | 18,288 | ₦14,630,400 |

| 3 | 22,483 | ₦17,986,400 |

| 4 | 27,454 | ₦21,963,200 |

| 5 | 31,011 | ₦24,808,800 |

| 6 | 34,948 | ₦27,958,400 |

This table shows how funds grow in both CAD and Naira as your family expands. Notice the jump of over ₦3.5 million between each additional member.

Translating Amounts Into Naira

To visualize these figures, imagine a bar chart comparing each CAD amount with its Naira counterpart at ₦800/CAD. Key data points include:

- ₦11.8 million for one person

- ₦21.9 million for a family of four

Seeing these bars side by side quickly reveals which family size demands the steepest savings growth.

Why These Figures Matter

These thresholds are based on Canada’s Low-Income Cut-Off (LICO), which draws on metrics like the Consumer Price Index and the Canadian Income Survey. For 2024, Express Entry proof-of-funds levels were set as a percentage of updated LICO values, ensuring newcomers arrive with enough buffer. Discover more about how LICO shapes requirements here.

Strategies To Build And Maintain Your Savings

Financial advisors recommend practical steps for hitting these targets despite naira volatility:

- Open a designated savings account with a high-interest option

- Automate monthly transfers of ₦200,000–₦300,000

- Use gift pooling from relatives, keeping a clear audit trail

- Diversify across fixed deposits and Forex wallets

- Track progress in a spreadsheet or mobile app, adjusting for rate changes

By following these tips, you can close the gap between your current savings and Canada’s CAD requirements. In the next section, we’ll cover the exact Nigerian bank documents you need to make your proof-of-funds application bullet-proof.

Documentation That Wins: Nigerian Financial Proof That Works

Moving from savings strategies to the actual paperwork, this section outlines the Nigerian bank documents that satisfy IRCC requirements. Too often, applicants submit generic bank statements lacking the precise terminology expected by both GTBank and Canadian visa officers. Getting your documentation right ensures every detail is clear and verifiable.

Case Studies: Letters That Impress Visa Officers

Analysis of successful Nigerian applicants highlights these Key Elements in a bank letter:

- Official Letterhead with branch stamp for authenticity

- Account details: account number, date opened, and current balance

- Six-month average balance to demonstrate steady funds

- Clear disclosure of outstanding debts for full transparency

These items match IRCC’s proof-of-funds checklist. Learn more by reviewing the official IRCC financial proof guidelines.

Templates for Major Nigerian Banks

JapaChat provides ready-to-use models for key banks:

| Nigerian Bank | Header & Stamp | Balance Details | Debt Disclosure |

|---|---|---|---|

| GTBank | Branch code, manager signature | Current & 6-month average | Itemized list |

| First Bank | Corporate letterhead, date | Daily balances summary | “No additional liabilities” |

| Zenith Bank | Watermark, official seal | Month-end balances | Outstanding loans section |

Adapting these templates prevents vague statements, helping visa officers locate required information at a glance.

Supplementary Documents That Strengthen Your Application

Beyond your bank letter, consider adding:

- Investment Certificates (e.g., stocks, mutual funds) with purchase dates

- Property Valuations certified by a registered surveyor

- Fixed Deposit Slips showing maturities beyond travel dates

- Forex Wallet Statements to prove foreign currency reserves

Providing multiple proofs paints a fuller financial picture and reduces follow-up queries.

Main Takeaways And Next Steps

- Precision Is Paramount: generic documents won’t clear IRCC’s checklist

- Use Bank-Specific Templates to align Nigerian formats with Canadian standards

- Supplement With Other Assets for a well-rounded profile

With spot-on documentation in hand, you’ll move confidently to the next stage. In Section 4, we’ll examine common financial red flags in Nigerian applications and how to avoid them.

Why Nigerian Applications Get Rejected: Financial Red Flags

Most Nigerian applicants believe that showing a high balance in their bank statement is enough. However, proof of funds documentation must demonstrate consistent savings, clear sources, and reputable banking practices. Visa officers evaluate more than just totals—they inspect transaction histories, inflows, and account credibility.

When local habits such as informal loans or pooled family savings go unexplained, they can be misread as attempts to inflate balances. Understanding these financial red flags and preparing clear explanations is crucial for a successful application.

Unexpected Transaction Patterns

Sudden, ₦3 million deposits far above the six-month average often appear as last-minute efforts to boost balances. For instance, a large inflow six weeks before the application may seem unsubstantiated. To address this:

- Maintain regular monthly deposits.

- Prepare invoices, pay slips, or sale receipts to verify each major transaction.

Informal Banking Practices

Many applicants use mobile money wallets, POS agents, or community loan schemes, which may lack official stamps or letterhead. Visa officers may question the legitimacy of these statements. To avoid this:

- Transfer informal funds into a recognized bank account at least two months before applying.

- Obtain an official bank letter outlining account opening dates and average balances over the past six months.

Family-Pooled Resources Without Clarity

Pooling funds from relatives is common, but undocumented gifts or loans can prompt suspicion. Officers might view these contributions as unsupported largesse. To clarify:

- Provide signed gift letters for each contribution.

- Include proof of relationship and account statements for all contributors.

Prevention Strategies

- Automate transfers so your six-month average never falls below ₦800,000.

- Request detailed bank letters on official letterhead, including account opening dates and average balances.

- Translate informal or investment documents into English with notarized summaries.

- Maintain an audit trail for every large deposit or family contribution.

Common Rejection Reasons And Prevention Strategies

A comparison of frequent reasons Nigerian applications are rejected based on proof of funds issues and practical strategies to avoid these problems

| Rejection Reason | Why It Happens | Prevention Strategy |

|---|---|---|

| Sudden Large Deposits | Deposits exceed typical six-month averages without proof | Provide invoices, salary slips, or sale contracts |

| Informal Savings Channels | Statements lack official bank stamps or letterhead | Move funds into formal bank accounts at least two months prior |

| Unexplained Family Contributions | Absence of gift letters or relationship documentation | Submit signed gift declarations and contributors’ bank statements |

| Inconsistent Average Balances | Recent withdrawals or irregular transfers reduce clarity | Automate monthly deposits to maintain steady balances |

This table underscores the importance of transparent financial records. By addressing each rejection reason with clear documentation, applicants can significantly reduce the risk of visa denials.

Read also: How to master visa interview questions and answers

Legitimate Money Sources: What Canada Accepts From Nigerians

When you prepare your proof of funds Canada package, the source of each naira matters as much as the total amount. A regular salary from a registered Lagos employer usually clears immigration checks, while large amounts of unverified cash may invite extra questions. Knowing which income streams Canada considers reliable will help you avoid delays.

Recognised Income Streams

Canadian visa officers typically accept funds from:

- Registered Employment Income: Payslips and official bank transfers

- Rental Income: Tenancy agreements and deposit records

- Family Business Profits: Audited accounts or corporate bank statements

- Sale of Property: Land registry receipts and notarised sale agreements

- Investment Dividends: Share certificates and brokerage statements

- Gifts From Relatives: Signed gift letters and contributor statements

Each category must be backed by clear documentation that shows you legally own or control the funds.

Documenting Funds From Family Businesses

If your family’s garment shop in Kano finances your application, gather:

- A letter on official letterhead from the company

- Details of six-month average balances in the business’s bank account

- A copy of the latest tax clearance certificate

- A board resolution or shareholder minutes authorising the transfer

This package offers transparency and meets Canadian requirements.

Tracing Proceeds From Property Sales

When you sell land or a house, include:

- Land Registry Documents showing transfer of title

- Receipts for all down payments

- A notarised affidavit confirming the sale price

- Bank statements showing the deposit into your account

An independent valuation report can further strengthen your case.

Handling Informal Sector And Currency Conversions

Many Nigerians earn via POS services or mobile wallets. To legitimise these funds:

- Transfer informal earnings into a recognised bank account at least two months before applying

- Obtain formal transaction receipts from your bank teller

- Keep forex documentation if you convert naira to CAD

Best practices include:

- Automating monthly transfers

- Using a dedicated “immigration” account

- Retaining all cheques and swap receipts

Comparison Of Source And Documentation

| Source | Acceptable Proof | Notes |

|---|---|---|

| Employment Salary | Payslips, bank statements | Show consistency over 6 months |

| Rental Income | Tenancy agreement, deposit records | Highlight monthly rent inflows |

| Family Business | Audited accounts, tax certificates | Must be on official letterhead |

| Property Sale | Land registry, sale receipts | Include affidavit and valuation report |

| Informal Earnings | Formal bank receipts, forex swap tickets | Transfer at least 60 days before submission |

You might be interested in: Check out our guide on Applying for Permanent Residence in Canada.

With these documented sources, you’ll meet Canada’s transparency standards and reduce follow-up queries. In the next section, we’ll explore how to build a robust financial profile that strengthens your entire application.

Building Your Financial Profile: Nigerian Success Strategies

Meeting the minimum proof of funds Canada threshold is only the first step. Nigerians face double-digit inflation and daily naira volatility. By pairing timely savings with recognised investment vehicles and organised documentation, you can offer visa officers a clear, reliable financial narrative. This approach shows that your funds are stable and legitimately sourced.

Timing Your Fund-Building Strategy

Successful applicants recommend aligning your savings with exchange-rate patterns:

- Automate ₦500,000 monthly transfers into a dedicated “immigration” account.

- Monitor naira/CAD spot rates and increase deposits when they ease by 5–10%.

- Stagger major contributions over 4–6 months to maintain a consistent balance.

By spreading deposits, you sidestep large last-minute inflows that may raise questions and build a clear upward trend in your account.

Leveraging Nigerian Investment Vehicles

Local markets provide instruments that translate smoothly into Canadian proof:

| Investment Vehicle | Expected Return | Liquidity | Supporting Document |

|---|---|---|---|

| Domiciliary Account | 0–1% (USD holdings) | High | Official bank statement |

| Commercial Fixed Deposit | 7–10% APR | Medium (90 days) | Maturity certificate |

| CBN Treasury Bills | 11–13% yield | Low (91 days) | Broker-issued certificate |

| Real Estate Fund | 8–12% p.a. | Low–Medium | Independent valuation report |

Combining these options boosts your naira savings and creates the official paperwork that IRCC officers recognise.

Building Banking Histories That Inspire Confidence

A transparent banking record reduces delays and inquiries:

- Use one or two main accounts rather than multiple small ones.

- Request six-month average balance letters in clear English, with branch stamp and manager signature.

- Keep transaction receipts and add brief notes for any large deposits.

A tidy history of regular balances and legitimate sources makes it easier for officers to approve your application.

Collaborative Funding: Family Sponsorship & Resource Pooling

If personal savings fall short, pool funds in line with IRCC guidelines:

- Collect contributions from relatives with signed gift letters.

- Establish a family trust and include board resolutions for each transfer.

- Attach each contributor’s relationship proof and six-month bank history.

| Method | Description | Key Documentation |

|---|---|---|

| Gift Letter Pooling | Relatives gift funds formally | Signed letters, IDs |

| Family Trust Arrangement | Legal trust holds and disburses funds | Trust deed, trustee letters |

| Joint Account Declaration | Multiple family members on one account | Account mandate, statements |

These methods respect local customs while meeting Canadian evidence rules.

Main Takeaway

By combining timed transfers, recognised investment instruments, and clear documentation, you turn naira volatility into a structured financial story. This strategy not only fulfils the proof of funds Canada requirement but also strengthens your overall application.

For personalised guidance on your Canadian journey, try JapaChat — Nigeria’s AI immigration expert platform with over 10,000 Nigerians already on their way abroad. Get free checklists and instant answers today.

Leave a Reply