Proof of Funds for Canada: Essential Tips & Requirements

Submitting your proof of funds for Canada is much more than just ticking a box on your application. Think of it as your financial launchpad, showing Immigration, Refugees and Citizenship Canada (IRCC) that you’re truly ready to build a new life here and can hit the ground running without immediate money worries.

Why Proof of Funds Is a Deal-Breaker

Let’s get one thing straight: showing you have the required settlement funds isn’t just another piece of paperwork. For an IRCC officer, it’s a critical sign of how well you're likely to settle in Canada. It's a safety net designed to make sure you can cover those initial, and often expensive, costs like your first month's rent, groceries, and transportation while you get on your feet.

This requirement is really about setting you up for success. Having those funds ready and available means you can focus on the important things, like finding a great job and settling into your new community, without the crushing stress of a financial crisis.

Which Immigration Programs Have This Requirement?

Whether you need to show proof of funds really boils down to the specific immigration program you’re applying through. For most of the economic immigration streams, it’s an absolute must.

You'll almost certainly need to provide proof of funds for these key programs:

- Federal Skilled Worker Program (FSWP): If you're applying through this popular Express Entry stream, showing you have the minimum settlement funds is mandatory.

- Federal Skilled Trades Program (FSTP): Just like with the FSWP, skilled trades applicants need to prove they have the financial resources to support themselves.

- Most Provincial Nominee Programs (PNPs): While the exact rules can differ from one province to another, the vast majority of PNPs will ask for settlement funds, especially if you’re coming through an Express Entry-linked stream.

The thinking behind this is pretty simple: it protects both you and the Canadian system. The government wants to see that newcomers can support themselves initially without needing to rely on social assistance. This ensures a smoother start for you and a positive contribution to the economy from the get-go.

Now, not everyone has to jump through this hoop. The biggest exception is for those applying under the Canadian Experience Class (CEC). If you have recent Canadian work experience, IRCC generally trusts that you've already proven you can integrate into the job market, so proof of funds isn't required. Similarly, applicants who already have a valid, arranged job offer in Canada are often exempt.

The logic here is all about assessing your readiness. If you've already worked in Canada or have a job lined up, you've already cleared a major settlement hurdle. You can learn more about why this financial vetting is so important by reading up on the proof of funds for Canada PR process.

Calculating How Much Money You Actually Need

Getting the proof of funds calculation right is one of the most critical parts of your application. This isn't just a number plucked out of thin air; it’s a specific amount tied directly to your family size, designed to ensure you can support yourself and your family upon arrival. The figure is based on 50% of the Low Income Cut-Off (LICO) totals—essentially, the poverty line in Canada.

One of the biggest tripwires for applicants is understanding who counts as a family member. It’s broader than you might think. Immigration, Refugees and Citizenship Canada (IRCC) includes you, your spouse or common-law partner, your dependent children, and even your spouse's dependent children.

Crucial Point: You have to include all these family members in your calculation, even if they aren’t coming to Canada with you. This is a common and costly mistake. For example, if you are a family of four but one child is staying behind to finish school, you must still show funds for a family of four.

Understanding the Official Requirements

These financial requirements are a moving target. To reflect the current cost of living, IRCC updates the required amounts every year. This makes it absolutely essential to check the official IRCC website for the latest figures right before you submit your application. What was correct six months ago might not be today.

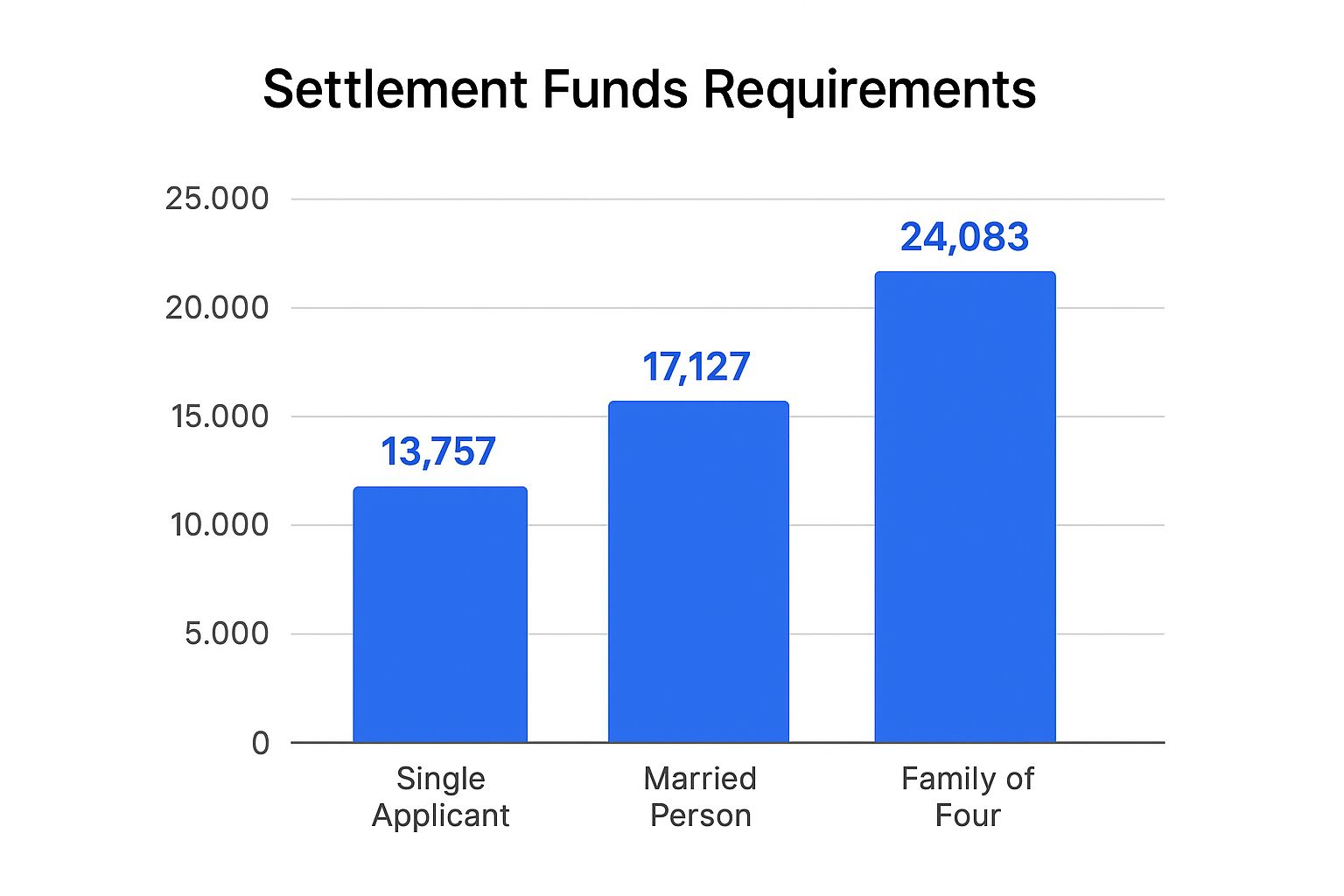

The table below shows the minimum funds you need to have. The amount is based on the size of your family and these figures are updated annually by IRCC.

Minimum Settlement Funds Required for Express Entry

| Number of Family Members | Funds Required (in CAD) |

|---|---|

| 1 | $14,690 |

| 2 | $18,288 |

| 3 | $22,483 |

| 4 | $27,297 |

| 5 | $30,690 |

| 6 | $34,917 |

| 7 | $38,875 |

| For each extra member | +$3,958 |

Remember, these are the absolute minimums. An officer needs to be convinced you can genuinely support your family, so having a bit more than the required amount is always a good strategy.

Here's a visual breakdown to help you see how the funds scale with your family size.

As you can see, the required amount increases significantly with each additional family member, reinforcing why an accurate calculation is so important.

Putting It All Together

Let's look at a practical example. Say we have a family of four—a primary applicant, their spouse, and two children. Even if the younger child is staying behind with grandparents for a year, IRCC considers them a family of four for settlement fund purposes. This means they need to prove they have at least $27,297 CAD ready and available.

Meeting the minimum is just one piece of the puzzle. It’s also wise to research the average salary expectations in Canada to create a realistic long-term budget. Your proof of funds gets you in the door, but smart financial planning is what will help you build a successful new life.

What Counts as Proof of Funds (and What Doesn't)

When you're preparing your https://blog.japachat.com/proof-of-funds-canada/, it's critical to understand that not all money is viewed the same way by an IRCC officer. The golden rule here is liquidity. Your funds must be readily available to you, with no strings attached.

This means you can't count assets like property or a car. The same goes for money tied up in stocks, bonds, or mutual funds—unless you've sold them off completely. The cash has to be sitting in your account, free and clear, before you can count it towards your settlement funds.

Getting the Official Bank Letter Right

A simple bank statement from an ATM won't cut it. What you need is an official letter from your bank, printed on their official letterhead. This document is your primary piece of evidence, and it needs to be flawless.

To be considered official, the letter from your bank must include:

- The financial institution's complete contact details (address, phone, and email).

- Your full name, clearly stated as the account holder.

- A comprehensive list of any outstanding debts or loans you have with them.

- The specific details for every current chequing, savings, or investment account.

For each account listed, the letter must show the account number, the date it was opened, the current balance, and—this is key—the average balance over the last six months. This six-month history is non-negotiable; it proves to the immigration officer that the money is genuinely yours and wasn't just borrowed and deposited last week to meet the minimum requirement.

A weak, generic statement just shows a snapshot in time. A strong, detailed letter tells the full story of your financial stability, leaving no room for an immigration officer to have doubts.

Acceptable vs. Unacceptable Funds: The Bottom Line

Let's be crystal clear about what works and what will get your application flagged. Borrowed money is an immediate red flag. This includes personal loans, lines of credit, or even a large "gift" from a friend or family member that looks like a loan. You have to be the undisputed owner of the funds.

So, what can you use?

- Savings Accounts: The most straightforward and common source.

- Chequing Accounts: Funds you can access on demand.

- Guaranteed Investment Certificates (GICs): Acceptable only if they are cashable or redeemable.

- Term Deposits: Like GICs, these are fine as long as you can liquidate them easily.

While your main goal is to satisfy IRCC, getting these documents in order now has other benefits. You’ll find that understanding financial requirements for rental applications in Canada is much easier when you've already done this homework. Landlords often ask for similar proof of financial stability, so you'll be one step ahead when it's time to find a place to live.

Getting Your Financial Paperwork in Order

https://www.youtube.com/embed/PDPywsQviN8

Alright, enough with the theory. Let's get down to the practical steps of pulling together your financial documents. This part of the process is all about being meticulous. Think of it as building a case for your financial stability, where every document adds another piece of solid evidence. Your goal is to be so clear and organised that the immigration officer has zero questions.

The most important piece of this puzzle is an official letter from your bank. This isn't just any printout; it has to be on the bank's official letterhead and include their full contact information. This letter is the foundation of your entire proof of funds submission.

What Your Bank Letter Absolutely Must Include

When you walk into your bank or contact your representative, you need to be specific. Don't just ask for a "proof of funds letter" and hope for the best. You'll save yourself a world of headaches and potential delays by giving them a precise checklist of what IRCC requires.

Make sure the letter explicitly states the following:

- Your full name (matching your application, of course).

- A complete list of all your current chequing and savings accounts.

- The exact account numbers for each of these accounts.

- The date each account was opened.

- The current balance in each account as of the letter's date.

- The average balance for the past 6 months for each account.

That 6-month average balance is non-negotiable. It's how the officer verifies that your funds are genuinely yours and have been stable over time—not a last-minute loan from a relative to pad your account. For a deeper dive into what makes this document so persuasive, it's worth understanding the anatomy of a strong Proof of Funds (POF) letter.

Dealing with Translations and Digital Submissions

What if your bank statements are in a language other than English or French? Simple: you'll need them professionally translated. Every document you submit must be accompanied by a certified translation, which includes the original document, the translated version, and an affidavit from the translator.

A word of advice from experience: Don't put this off. Certified translators are often booked up, and a rushed job can introduce small but critical errors that could put your entire application at risk. Start this process early.

Once your papers are sorted, it's time to prepare them for digital upload. This is where many applicants trip up. IRCC has specific guidelines, and just dumping your files with names like "Scan1.pdf" is a recipe for confusion.

Be descriptive and organised. A file name like "MainApplicant_ProofOfFunds_BankLetter_May2024.pdf" makes life much easier for the officer reviewing your file. Also, double-check that your scans are crystal clear and easy to read. These small details show you're a serious, organised applicant, which is a theme that runs through the entire application for PR in Canada process. A little bit of organisation now will save you a massive amount of stress down the line.

Common Application Mistakes You Need to Avoid

It’s a tough reality, but a simple mistake with your proof of funds for Canada can bring your entire immigration dream to a screeching halt. Even with a perfect application in every other respect, an error in your financial documents can lead to a flat-out rejection. Knowing what these common pitfalls are is the best way to steer clear of them.

One of the biggest red flags for immigration officers is a sudden, large deposit into your account right before you apply. They’re specifically trained to look for this. If your bank balance shoots up from ₦2,000,000 to ₦15,000,000 overnight without a crystal-clear, documented explanation, they will immediately suspect the money is borrowed. That’s a deal-breaker.

The Problem with Borrowed Money

Let me be clear: IRCC is incredibly strict about this. Borrowed money is not acceptable. This covers everything from a line of credit or a bank loan to an informal loan from a family member. The money has to be yours, free and clear, and ready for you to use to support your settlement in Canada.

When you use borrowed funds, you’re sending a signal to the visa officer that you lack the financial stability needed to succeed. The whole point of showing settlement funds is to prove you won’t struggle financially when you land. Borrowed money completely defeats that purpose.

Documenting Large Gifts the Right Way

So, what happens if a parent or another family member gives you a large sum of money as a genuine gift? That can be okay, but you have the responsibility to prove it’s a true gift, not a loan disguised to meet the requirement. Just having the money appear in your account isn't going to cut it.

For a gift to be accepted, you need to provide solid proof:

- A formal gift deed: This is a signed, legal letter from the person giving you the money. It must explicitly state the funds are a gift, not a loan, and that they have no expectation of you ever paying it back.

- Proof of the transaction: You need to show the complete paper trail. This means bank transfer slips, a statement from the giver's account showing the money leaving, and your bank statement showing the same amount arriving.

Without this airtight documentation, the funds will be viewed with suspicion. Remember, the burden of proof is always on you to be transparent and thorough.

A lot of applicants make the mistake of thinking a simple letter of explanation is sufficient. You really need both the formal gift deed and the transaction records to build a case that leaves no room for an officer's doubt.

Inconsistent Financial History

Another mistake I see all too often is failing to keep the required balance consistently. That six-month history rule isn't a suggestion; it's a fundamental part of the review process. An officer will look at your average balance over that entire period to confirm the funds are stable and truly belong to you.

Dipping below the required minimum, even for just a few days within those six months, can be a major problem. It suggests the funds might not be fully at your disposal. Your financial history needs to tell a consistent story of stability. As you gather your documents, remember you're not just providing a snapshot of your account today; you're building a financial narrative that supports your entire immigration goal. Getting these details right is a crucial part of creating an Express Entry profile that leads to an approval.

Common Questions We Hear About Proof of Funds

Working through the proof of funds requirement for Canada can feel a bit like navigating a maze. Just when you think you have it all figured out, a specific situation pops up and you're left wondering. Let's clear the air and tackle some of the most common questions we see from applicants.

One of the first things people ask is about getting a little help from family. Can that generous gift from your parents count towards your settlement funds? The short answer is yes, but it comes with a strict process you absolutely have to get right.

A simple bank transfer won’t cut it. For a monetary gift to be accepted, you need to treat it as a formal, documented transaction. This means getting a signed gift deed – a legal letter from your parents confirming the money is a genuine gift and not a loan they expect back. You’ll also need to show a clear paper trail, from the transaction record of the money leaving their account to it landing safely in yours. Without this, an officer is likely to view it as a loan and reject those funds.

What if I Already Have a Job Offer in Canada?

This is where things can get a little tricky, and the answer really depends on the specific immigration program you’re using. It’s a common mistake to assume a Canadian job offer automatically means you don't need to show any settlement funds. That assumption can be a costly one.

If you're applying under the Canadian Experience Class (CEC), you're generally in the clear. Your work history in Canada is seen as proof you can support yourself. However, for those in the Federal Skilled Worker Program (FSWP) or the Federal Skilled Trades Program (FSTP), the story is different. Even with a valid Canadian job offer, you’ll almost always still need to show you meet the minimum funds requirement.

Here's a real-world scenario we see often: An applicant has foreign work experience and a Canadian job offer, so they qualify for both CEC and FSWP. If an officer assesses their application and finds a small issue with their CEC eligibility, they'll pivot to assessing it under FSWP. If you haven't included your proof of funds, your application will be dead in the water right there. It's always safer to have it ready.

How Long Do I Need to Have the Money in My Account?

You’ve probably heard people mention a "six-month rule." While you won't find that exact phrase on the IRCC website, it’s a golden rule to live by. Immigration officers will want to see your financial history for at least the six months right before you apply. Why? They need to confirm the money is genuinely yours, stable, and wasn't just borrowed last-minute to tick a box.

This look-back period gives them the full picture of your financial situation. They’re looking for stability—proof that the funds have been yours over a reasonable period, not just deposited last week. Any sudden, large deposits are a huge red flag unless you back them up with solid proof, like that gift deed we talked about. Think of your bank statements as telling the story of your financial readiness to start a new life in Canada.

Planning your move abroad can be complex, but you don't have to do it alone. JapaChat is Nigeria's first AI immigration expert, designed to give you instant and accurate answers to all your questions. Get the clarity and confidence you need by signing up for free.

Leave a Reply